ChatGPT can read bank data, and finance AI starts with read-only trust

OpenAI brought personal finance into ChatGPT. The real story is not budgeting, but how AI products handle permission boundaries around sensitive money data.

- What happened: OpenAI launched a

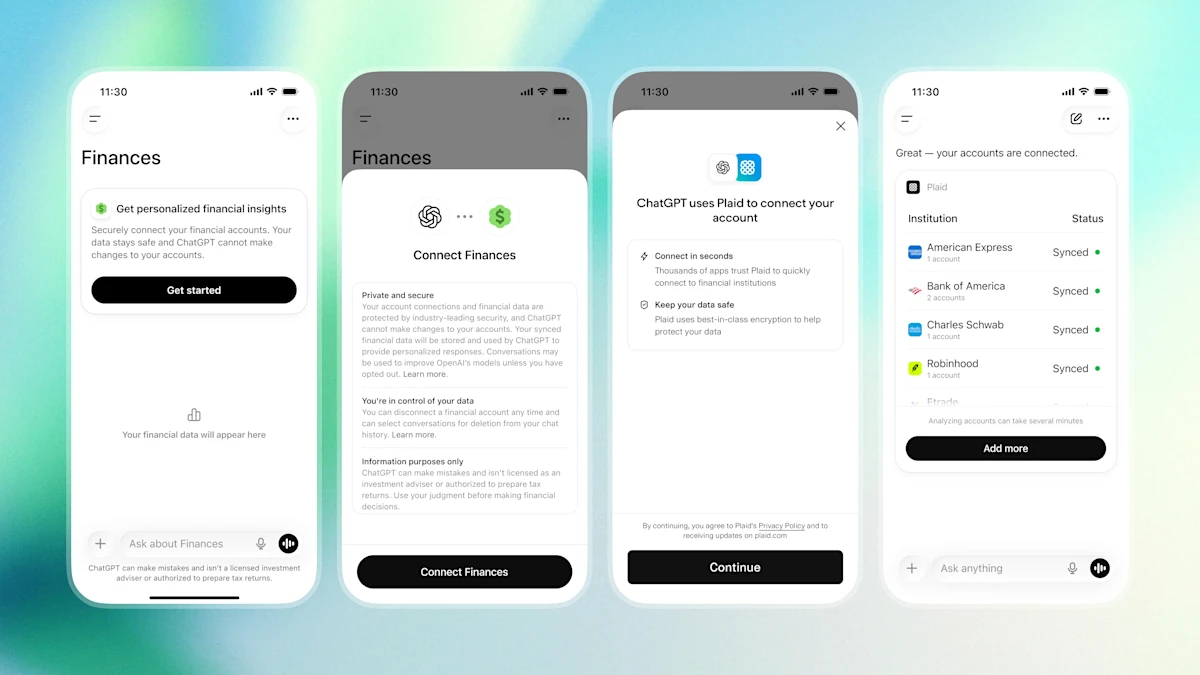

Financespreview for U.S. ChatGPT Pro users.- Users can connect accounts from more than 12,000 financial institutions through Plaid and ask ChatGPT about spending, subscriptions, net worth, investments, and debt.

- The boundary: ChatGPT can read financial data, but it cannot move money, pay bills, trade, change account settings, or file taxes.

- OpenAI is emphasizing read-only access, 30-day deletion after disconnect, and a clear disclaimer that ChatGPT is not a financial adviser.

- Why it matters: The AI product contest is shifting from answer quality to sensitive data permission design.

- Watch: OpenAI's Intuit examples show that financial AI may move from answers into partner-mediated action workflows.

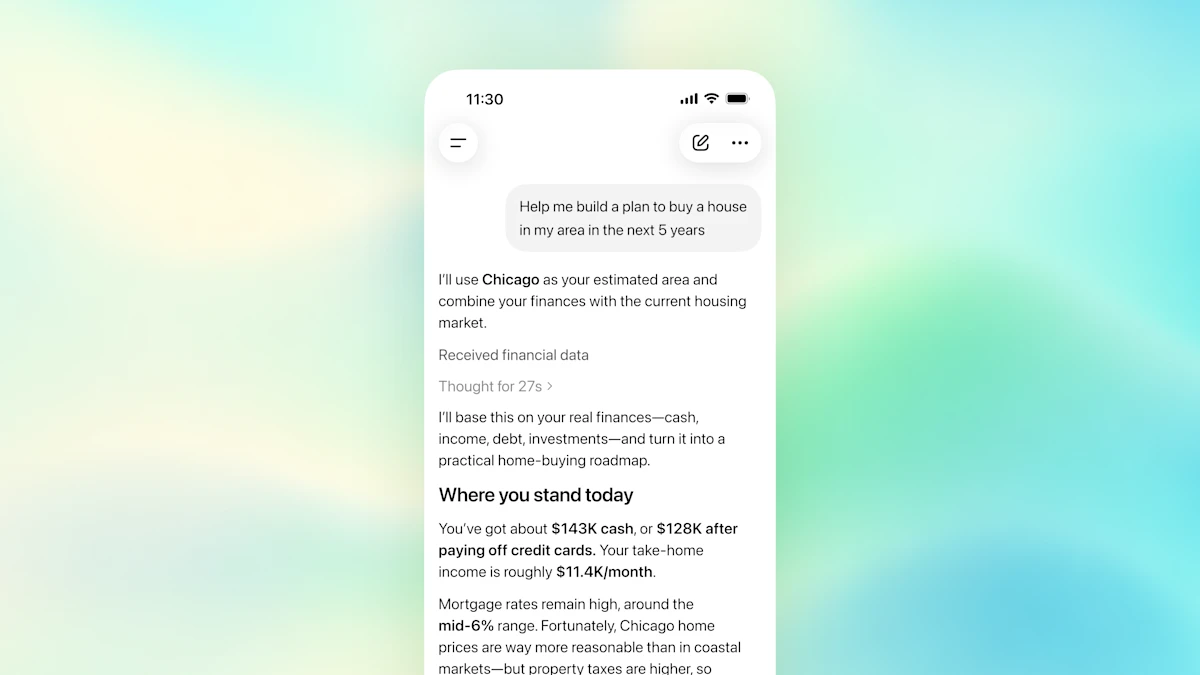

OpenAI has put personal finance inside ChatGPT. In a May 15, 2026 announcement, the company said U.S. ChatGPT Pro users can begin using a Finances preview on web and iOS. Through Plaid, they can connect bank, credit card, brokerage, and loan accounts, then ask ChatGPT questions such as why spending went up this month, where subscriptions are leaking money, or how much they need to save to buy a home within five years.

If this news is read only as "ChatGPT added a budgeting feature," the important part disappears. OpenAI is not just adding a spreadsheet-like consumer app. It is touching the interface for personal financial data. Until now, ChatGPT could give advice based on information a user typed in, uploaded, or retrieved from the web. With account linking, it can pull changing data such as balances, transactions, investments, and liabilities. AI is getting a direct view into the flow of a person's money.

At the same time, OpenAI put strict limits around the feature. The Help Center document says ChatGPT cannot send money, pay bills, change account settings, trade securities, change retirement contributions, open or close accounts, or file taxes. The company also repeats that ChatGPT is not a financial, legal, tax, or investment adviser, and that users remain responsible for their decisions.

That makes the core question sharper. Before AI moves money, how much permission should it have to understand money?

Two hundred million finance questions become a product surface

OpenAI says more than 200 million people ask ChatGPT finance-related questions each month. Those questions cover budgeting, investing, comparing options, and planning future goals. That number is the strongest explanation for the launch. Users were already bringing sensitive money problems into a general-purpose chatbot, and OpenAI is now turning that behavior into a dedicated product surface.

The old ChatGPT could already answer "How can I reduce spending?" Without connected data, however, the answer usually stayed generic: eat out less, review subscriptions, automate savings, build an emergency fund. Those suggestions can be sensible, but they are distant from a user's real account activity. Finances tries to close that gap. Once accounts are connected, ChatGPT can reason over recent transactions, recurring payments, balances, portfolio composition, and liabilities.

OpenAI's own examples show the difference. Before connection, the assistant might give general guidance on saving more over three months. After connection, it can look at spending categories from February through early May and suggest a concrete plan to cut $500 to $750 per month across dining, shopping, transportation, and groceries. The user's financial life becomes model context. The chatbot starts to look less like a generic adviser and more like a reasoning layer on top of a personal dashboard.

For developers, the shift is broader than finance. The era when an AI app could differentiate mainly through a clever prompt or a stronger model is narrowing. Product value increasingly comes from which sensitive data the system can access, under what authority, with which deletion policy, memory behavior, audit trail, and fallback path. Finance, health care, workplace documents, and developer infrastructure are all moving in that direction.

Plaid is the connector, and Intuit is the signal

The first account-linking partner is Plaid. OpenAI says the preview supports more than 12,000 financial institutions. TechCrunch reported examples such as Schwab, Fidelity, Chase, Robinhood, American Express, and Capital One. A user can start from the Finances section in the ChatGPT sidebar or type @Finances, connect my accounts in a conversation to begin the linking flow.

Plaid is not a new infrastructure layer. Many budgeting, investing, and fintech products already use it to connect accounts without each app building separate integrations to every bank. In that sense, OpenAI did not directly integrate 12,000 institutions by itself. It placed ChatGPT on top of an existing financial data network.

The ChatGPT surface still changes the user experience. A budgeting app often shows a dashboard and leaves the user to interpret it. ChatGPT receives a question, interprets the transactions, combines them with the user's goals and memories, and returns a natural-language conclusion. The same Plaid connection feels different when the user is not just looking at charts, but asking an AI that appears to understand their money. That is why the trust problem becomes larger.

The more important clue is Intuit. OpenAI says it is working with ecosystem partners such as Intuit on experiences that move from answers toward action. The announcement gives examples such as understanding credit card approval odds and submitting an application, or asking about the tax impact of selling stock and then moving toward a tax estimate or a local expert. Today's Finances preview is read-only, but the product vision clearly points toward action.

That is where the agent discussion enters. An agent is not merely a system that summarizes information. It accepts goals, calls tools, and changes outcomes. In finance, changing outcomes means touching money, credit, taxes, legal obligations, and liability. OpenAI's emphasis on a read-only safety line makes sense. If the first preview had opened execution permissions, the launch would likely have been dominated by regulation, responsibility, and security questions before users could even evaluate the product.

| Area | Current Finances preview | Action layer OpenAI is signaling |

|---|---|---|

| Permission | Reads balances, transactions, investments, and debt for answers | Connects to external flows such as card applications, tax estimates, and expert booking |

| Safety line | No transfers, trades, tax filing, or account changes | Partner consent, verification, and regulated handoff become central |

| Product value | Uses real financial context to interpret budgets, spending, goals, and risk | Shortens the workflow from question to execution |

| Risk | Data exposure, incorrect categorization, over-trust, and memory management | Wrong actions, unclear liability, regulatory fit, fraud, and account takeover |

Benchmarks do not replace trust

OpenAI says the finance experience uses GPT-5.5 Thinking by default. According to the announcement, OpenAI worked with more than 50 financial professionals to evaluate difficult personal finance tasks. On its internal benchmark, GPT-5.5 Thinking scored 79, while GPT-5.5 Pro scored 82.5. OpenAI describes the score as a weighted measure of answer quality and accuracy evaluated by experts.

Those numbers matter, but they are not enough. Finance questions are not just arithmetic. Income, spending, debt, cash balance, taxes, family obligations, goals, and timing can all interact. A question like "Should I build an emergency fund first or pay down credit card debt?" does not have a single universal answer. It requires assumptions and tradeoffs. Making GPT-5.5 Thinking the default suggests OpenAI sees this as a contextual reasoning problem, not a fast-answer widget.

Still, a benchmark cannot substitute for trust. First, this is an internal benchmark. Outsiders cannot easily know which tasks it includes or what user population it represents. Second, even a high score can hide serious tail risks. One bad interpretation of an individual's money situation can have real cost. Third, the financial data itself may be incomplete. The Help Center warns that some institutions may provide only balances and omit transaction history, investment holdings, loan details, APRs, or due dates.

OpenAI acknowledges some of this. Its documentation explains why a spending breakdown can be inaccurate: transfers, card payments, refunds, and pending transactions can be counted incorrectly, and AI can make mistakes. Users can ask which transactions were included, tell ChatGPT to reclassify items, and have those corrections remembered.

That creates an interesting product loop. If the AI is wrong, the user corrects it, and the correction becomes memory. A personal finance AI becomes not only a system that reads account data, but also a system that accumulates the user's interpretation of that data over time. That can make the product more useful. It also raises the stakes for deletion, portability, auditability, and explanation. If a user tells ChatGPT that a subscription is a business expense, how does that memory affect later advice? Where is it stored? What disappears when the account is disconnected, and what remains in conversation history?

Is data control clear enough?

OpenAI gives privacy and control a large section in the announcement. When accounts are connected, ChatGPT can access balances, transactions, investments, and liabilities, but OpenAI says it cannot see full account numbers or change accounts. If a user disconnects, synced account data is deleted from OpenAI systems within 30 days. Financial memories can be viewed and deleted from the Finances page. Temporary chats do not access connected financial accounts.

One important sentence is that finance conversations follow the user's overall ChatGPT data controls. In other words, this is not a completely separate learning and retention policy for finance. It is connected to the user's broader ChatGPT settings. If users do not understand that distinction, they may assume financial conversations are automatically excluded from model improvement or retention in a way the product does not actually guarantee.

Plaid-side data is a separate layer. The Help Center says Plaid will also delete data for the ChatGPT connection within 30 days according to policy after disconnect. But if a user has connected Plaid to other apps, those connections must be managed separately. This is realistic fintech infrastructure, but it complicates the user question: "If I disconnect in ChatGPT, is everything gone?" OpenAI, Plaid, banks, and future partners such as Intuit may each have separate data handling roles.

That helps explain why the community reaction was so sensitive. A Reddit r/technology thread showed strong distrust toward linking financial data to OpenAI or third parties, while r/OpenAI and r/ChatGPTPro discussions included reminders that Plaid-based read-only aggregation is common in finance apps. Both reactions can be reasonable. Plaid itself is familiar, but connecting that data to a general-purpose AI layer with memory and reasoning feels different from connecting it to a narrow budgeting dashboard.

Permission design is the product

For developers and AI product teams, the main thing to study is not the UI. It is the permission model. OpenAI is presenting account linking, data sync, financial memory, temporary-chat exclusion, 30-day deletion, MFA recommendations, professional-advice disclaimers, and execution limits as one package. That looks like an early checklist for AI products that handle sensitive data.

First, data access and action permission must be separated. A model's ability to see data does not imply it should be allowed to act on that data. ChatGPT Finances makes the split explicit: it can read, but it cannot move money. Health care, legal, HR, and developer infrastructure agents will face the same design pressure. An agent that reads server logs and an agent that changes production configuration belong in different risk classes.

Second, memory is both a feature and a risk. If a user says they owe money to family, plan to buy a car next year, or want to keep a minimum balance in checking, ChatGPT can store that as financial memory. With memory, advice becomes more personal. But sensitive information also becomes long-lived. A mature product must make the moment of memory creation, the deletion location, the status of conversation history after disconnect, and the limits of temporary chat understandable to users.

Third, explanations matter. OpenAI says ChatGPT can cite relevant source data when it uses connected financial information. That is not a small feature. If an assistant says grocery spending rose, the user needs to see which transactions were included, which were excluded, and which classifications may be wrong. Otherwise the user can only trust or distrust the answer. A correction loop needs visibility.

Fourth, benchmarks need external verifiability. OpenAI's 79 and 82.5 scores show direction, but financial AI needs more transparent evaluation if it is going to enter everyday use. Budgeting advice, investment risk explanation, tax concept explanation, debt repayment planning, suspicious transaction detection, and conservative answers under incomplete data should be evaluated separately. The question is not only whether the answer is accurate. It is also whether the system admits uncertainty, identifies situations that need professional advice, and avoids nudging users toward risky actions.

Read-only is the starting line

This preview is conservative, but that does not remove the risk. Read-only is the beginning of finance AI, not the end. If users feel that AI understands their spending accurately, the next requests will be obvious: cancel this subscription, move this money into savings, switch me to this card, book a tax consultation, rebalance this portfolio. OpenAI's Intuit examples show that the company is not hiding the direction.

At that point, product design becomes much harder. A credit card application is not just a link click. It involves credit data, income, legal consent, advertising relationships, conflicts of interest, and explanations of rejection risk. A tax estimate depends on jurisdiction, asset type, holding period, gains and losses, and personal circumstances. Investment-related advice touches regulation and suitability. The boundary between "the AI recommended this" and "the user chose this" becomes blurry.

That is why the finance AI race will not be decided by model performance alone. It will depend on who can build clearer permission requests, more conservative execution boundaries, better correction and deletion flows, more transparent partner disclosures, and more honest separation between general information and regulated advice.

OpenAI's launch is one more step toward ChatGPT becoming a personal operating layer. Codex connects to code and terminals. Workspace features connect to company documents and workflows. Finances now connects to personal money data. The question is the same in every domain: more context makes AI more useful, but more context also raises the cost of failure.

This time, OpenAI has made ChatGPT able to read the bank data. It still does not move the money. How clearly the product preserves that distinction may become the first real trust test for consumer finance AI.